Private Equity’s Growing Role in the Biopharma Industry

The bio/pharma industry, both bio/pharma companies and CDMOs/CMOS, has been a target of increased investment by private-equity (PE) firms. A recent analysis by Bain & Company examines financing trends and investments by PE firms, including how changes in financial markets and the biopharma industry’s supply chains ignited by the novel coronavirus pandemic could result in an even greater role for PE in biopharma in coming years.

PE investments in the biopharma industry

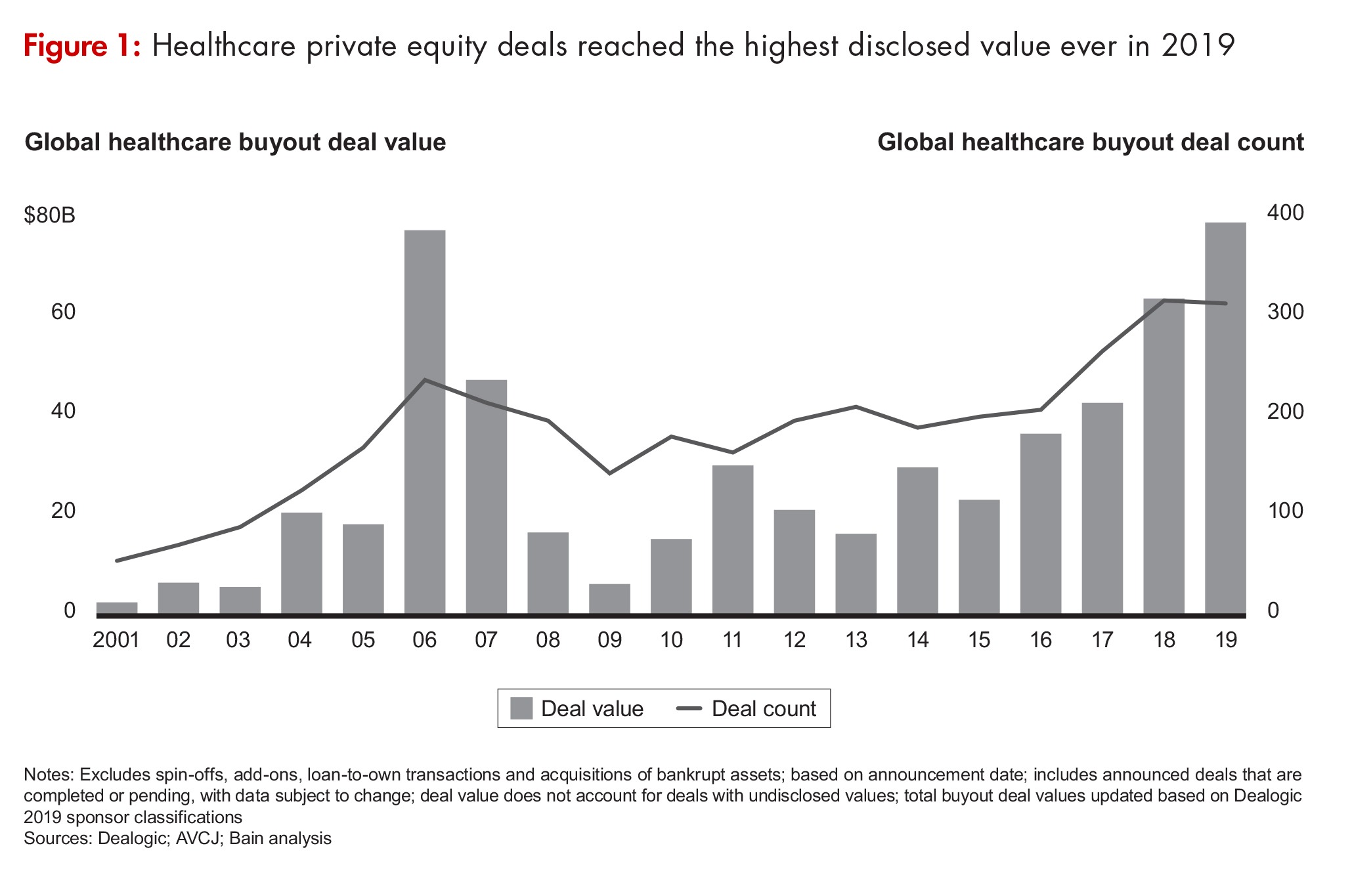

Private-equity (PE) investment in the biopharma industry (inclusive of both biopharmaceutical/pharmaceutical companies and CDMOs/CMOs to the biopharma industry) rocketed to $40.7 billion in 2019, two-and-a-half times the $16.5 billion that PE firms invested in the industry in 2018 (see Figure 1), according to Bain & Company’s Global Healthcare Private Equity and Corporate M&A Report 2020, which was published in March (March 2020). Bain & Company is a consulting partner to the PE industry and its stakeholders and separate from the investment activities of Bain Capital. PE consulting at Bain represents about one-quarter of the firm’s global business.

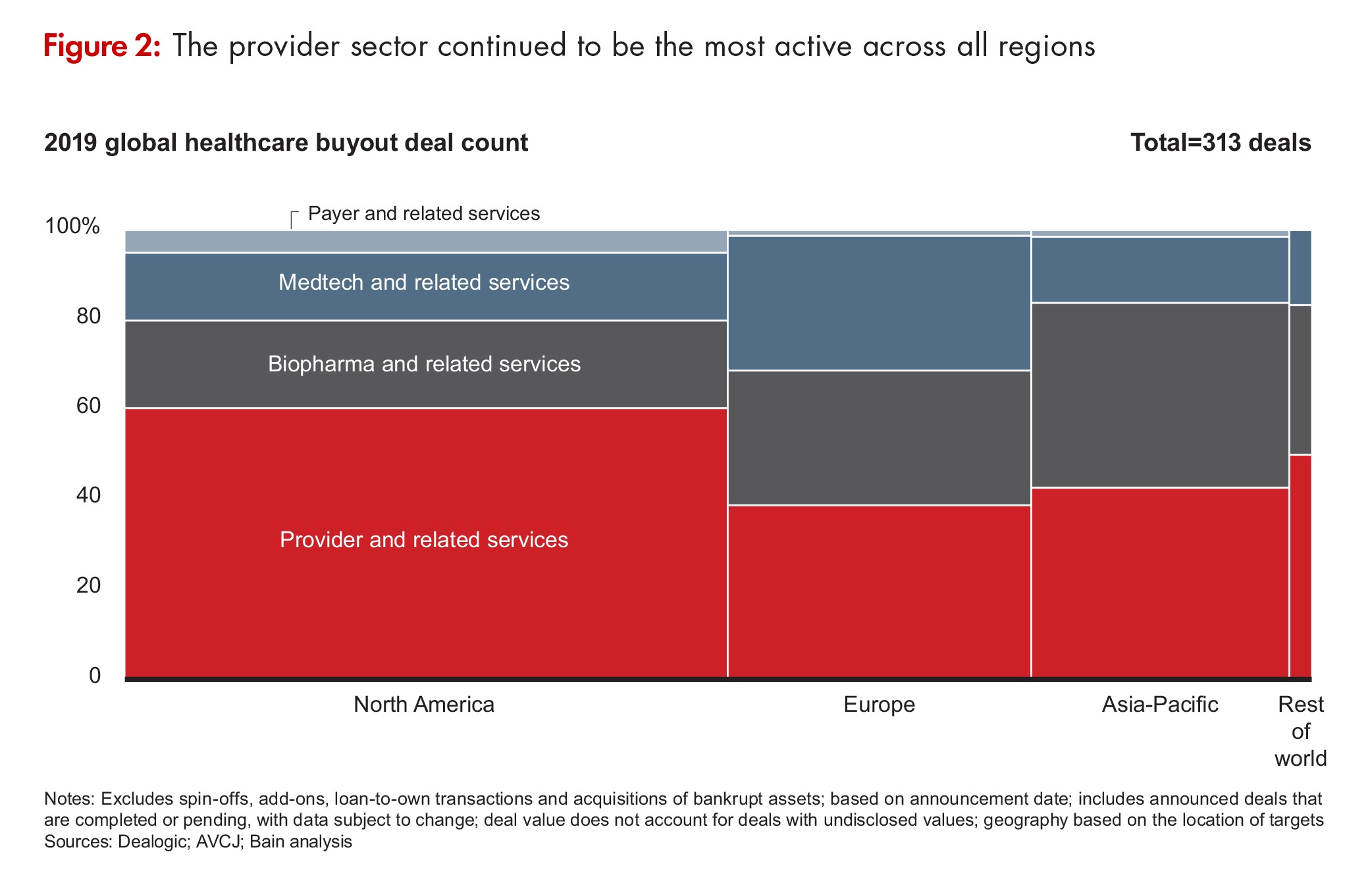

The 85 biopharma deals done by PE in 2019 included the $10.1-billion acquisition of Nestlé’s Skin Health business by the PE firm, EQT, and the Abu Dhabi Investment Authority. That deal alone accounted for 25% all of PE activity in biopharma in 2019 and was the single largest PE deal in healthcare. The $17.3 billion in investments in North American companies accounted for more than 50% of PE investments in biopharma when the Nestlé deal is excluded from the total.

Contract services were well-represented in the mix (see Figure 2). Permira’s $2.4-billion acquisition of Cambrex was the fifth-largest deal in all of healthcare in 2019 while the acquisition of Advarra, a provider of clinical research services, was the tenth largest at $1.5 billion. There were a number of smaller deals in the CDMO space, including those for Aldevron, a CDMO of DNA plasmid, protein, and mRNA production; Quotient Sciences, a CDMO of solid dosage forms and early-stage capabilities; and Vibalogics, a CDMO of therapeutic and prophylactic vaccines and biological products.

In fact, according to the Bain report, biopharma services and information technology to support drug development accounted for 51% of PE biopharma deals and 55% of deal value. Drivers for biopharma services investment include the desire to “ride the outsourcing wave,” and the opportunity to participate in the biopharma sector while evading pricing pressures on drugs. Investors also see substantial upside in new information technologies that can make clinical trials more efficient and can capture and process real-world data on drug use and outcomes to support drug development and outcome-based drug pricing.

Investing in drug development

The Bain report cited two other major themes in PE investing in biopharma: branded consumer and generic products; and early-stage investments in new product development. PE firms have bought into some well-known names in the mid-size and generic segments of the industry, including Zentiva (acquired by Advent International from Sanofi in 2018), Recordati (CVC Capital Partner acquired a controlling interest in Recordati in 2018), and Acino (acquired by Avista Capital and Nordic Capital in 2013) and those companies have themselves have been acquiring additional companies to build out their product lines and geographic scope.

|

|

Nirad Jain |

Still, the opportunities are nuanced and not across-the-board, says Nirad Jain, a Partner and Co-Head of Bain & Company’s Global Healthcare Private Equity practice. “’Generics’ is too broad of a category when looking for trends,” he says. “For example, specialty injectables are facing different market forces than retail oral solids, and therefore different investment opportunities. And branded generics outside of the US are very different than US generic oral solids. We see disruption and fundamental changes in market dynamics, which will create opportunities for new winners in the market.”

PE firms have also been investing directly in companies that are developing new drugs and are not yet generating commercial revenues. These include emerging biopharma companies that are typically the territory of venture-capital firms, and PE firms are also partnering with global biopharma companies to develop portfolios of new drug candidates that may have dropped in priority at the company. For instance, the PE firm, Blackstone, partnered with Novartis to create Anthos Therapeutics to develop a portfolio of Novartis cardiovascular candidates. Bain Capital and Pfizer established Cerevel to develop neurological candidates from Pfizer’s portfolio. In both cases, the biopharma company has contributed the candidates while the PE has put up the cash needed to fund candidate development.

Investment in early development is outside the normal investment philosophy of PE firms and would seem to carry a much dicier risk/reward profile. In fact, according to Jain, Bain’s analysis shows that PE returns for small biopharma investments (e.g., equity investments of less than $75 million) are in fact lower than those in more traditional opportunities.

Jain says that there are two forces driving this development. For one, the high levels of venture-capital investing in biopharma in 2018-2019 has created more opportunities for growth equity investments, i.e., investments in companies that have matured beyond their start-up phases and have promising products nearing approval.

Secondly, Jain says, is PE firms have raised large amounts of capital in recent years and that has led to intense competition that has driven up valuations of target companies. “There are record levels of dry powder’—or raised/committed, but yet-to-be-invested capital—in private equity,” Jain observes. “Combined with the increased and intense competition for healthcare assets, this is sending investors to parts of the investing spectrum where they have less direct investing experience.”

Investing in and with public companies has been another feature of PE investing in recent years. Avenues have included public-to-private transactions, such as Permira’s acquisition of Cambrex, and private investments in public companies (PIPES), such as Leonard Green’s investment in Catalent to help fund Catalent’s $1.2-billion acquisition of Paragon Bioservices, a CDMO of viral vector development and manufacturing services, in 2019.

Positive outlook

Jain foresees a positive outlook for PE investing in biopharma despite, and even thanks to, the financial crisis triggered by the novel coronavirus pandemic. He notes that biopharma has been the best performing sector of PE healthcare investments, with the best returns generated by very large investments (> $500 million) and small to mid-sized investments ($75–$150 million).

“The last recession in 2008/09 is instructive in a few ways,” Jain notes. “First, funds raised and investments made during the last recession delivered some of the best returns in private equity. Second, healthcare investments made during the last recession differentially outperformed returns in other sectors. So, we expect that the most sophisticated and successful investors to “double down’ on investing in this environment.”

PE investors have benefitted in recent years from multiple expansion, i.e., the willingness of investors to place a higher valuation on a given level of profitability or cash flow than they have in the past. That multiple expansion has led to positive investment outcomes even when company performance has not met expectations, but that may not be the case going forward.

“A very high percentage of investments—based on a rigorous analysis Bain performed on a representative sample of deals—miss their fundamental topline and/or margin growth goals as defined by the PE firm at the outset of their investment (i.e., in the deal model),” Jain warns. “In an expansionary market, these misses are often ‘covered up’ by multiple expansion. As we now enter a recessionary environment, these weaknesses will be exposed.”

Note: This article was developed based on Bain & Company’s scheduled participation in an education program at DCAT Week ’20, which was to have been held March 23–26, 2020 in New York.