Pandemic Complicates an Already Challenging Outlook for the Global Pharma Industry

The COVID-19 pandemic has greatly complicated an already challenging outlook for the global pharmaceutical industry. Graham Lewis, Vice President, Global Pharma Strategy, IQVIA lays out sales, cost, and supply impacts of COVID-19 on current and future industry performance.

Examining industry fundamentals

The COVID-19 pandemic has greatly complicated an already challenging outlook for the global pharmaceutical industry. Rising costs, slowing price increases, and deteriorating R&D productivity were already threatening industry performance. Now, the uncertainties surrounding vaccine availability and the long-term impacts on national healthcare systems will challenge pharmaceutical industry executives even more in coming years.

|

|

Graham Lewis |

That was the message conveyed by Graham Lewis, Vice President of Global Pharma Strategy for IQVIA to the online audience at DCAT’s Pharma Industry Outlook webinar held on June 30 (June 30, 2020). Lewis, has been the regular featured speaker at DCAT Week’s Pharma Industry Outlook education program since 2013, and his presentations are sought-after for their industry insights.

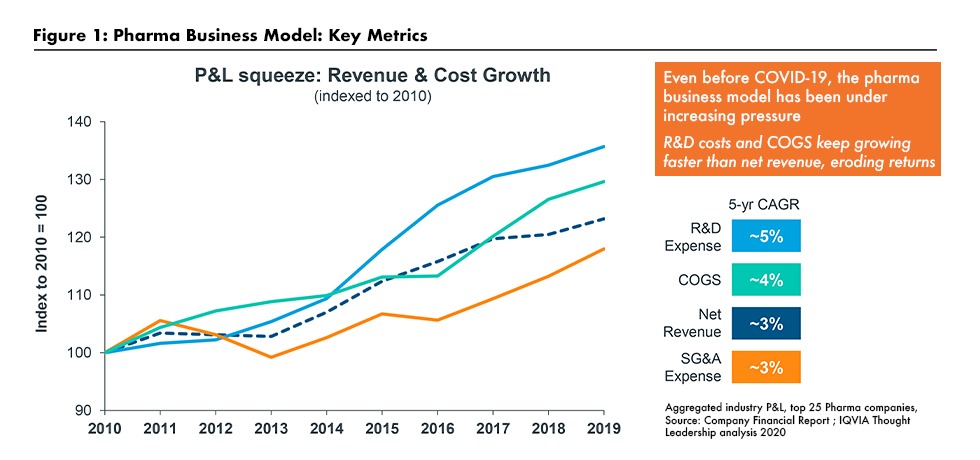

Even before the COVID pandemic, pharmaceutical industry executives were facing difficult strategic challenges, says Lewis. Profit margins were being compressed as annual cost increases, especially for cost of goods (COGS) and R&D, were outpacing growth in revenues (see Figure 1). According to a study produced by Deloitte and GlobalData and cited by Lewis, returns on investment in new product development for the 12 largest biopharma companies have fallen as R&D costs have risen and projected peak sales per new product have fallen.

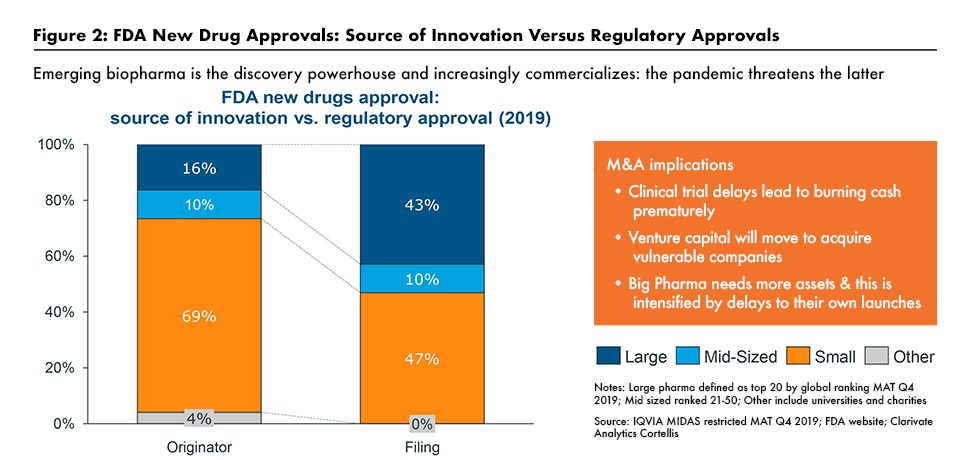

Emerging biopharma companies, which Lewis described as a “discovery powerhouse,” are increasingly intent at commercializing their own products (see Figure 2). Meanwhile, Chinese biopharma companies ae becoming a growing force in drug R&D, accounting for 10% of all candidates in the pipeline.

A big factor in the success of emerging biopharma companies has been the growth of specialty products, including products targeting cancer, diabetes, and autoimmune diseases; those products accounted for 40% of industry sales in 2019, double what they were in 2009. Specialty drugs target narrow indications, and their specificity make them less costly to commercialize and promote while capable of generating significant sales. Those characteristics pose a challenge for large pharma companies, noted Lewis, because they erode their scale advantages. He also noted that specialty products are becoming a bigger part of the mix in the largest emerging market countries, what he calls the “Pharmerging” countries, the BRICs, (Brazil, Russia, India, and China), Turkey, Mexico and more than 10 others representing the most attractive emerging markets for future growth.

The pandemic’s impact

The COVID-19 pandemic has greatly complicated the ability of global biopharma companies to address these challenges because of its impact on the health delivery system, says Lewis. Interactions between physicians and patients are down sharply despite the growing use of telemedicine, as are the volume of diagnostic procedures. As a result, the number of new prescriptions issued have declined significantly. Further, clinical trials have been slowed or delayed because of the inability or unwillingness of patients and trial monitors to reach clinical sites. Innovations, such as remote monitoring and direct-to-patient drug delivery, as well as relaxed regulations, have helped but have not fully alleviated the problem.

A further complication has been the reduced ability of drug company field sales staff to interact with physicians and other decision-makers. Detailing activity has declined as much as 50% in the major developed markets of the US and Europe, where online interactions have only marginally offset the reduction in face-to-face interactions between drug reps and providers. Those difficulties are, among other negative impacts, slowing the introduction of newly launched medications, which depend heavily on physician education.

Working off the backlog of patient visits and diagnostic and surgical procedures will be a gradual process so as not to stress healthcare systems even further, says Lewis. Clinical trials are getting back on track as sites gradually re-open, but difficulties will remain in recruiting certain subject cohorts such as older patients. As a result, drug launches and sales will be slowed for several more years.

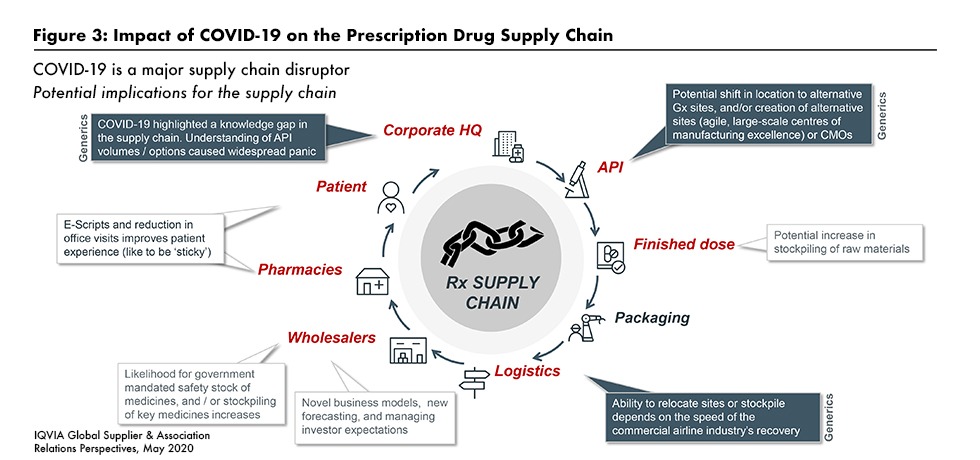

Difficulties in the drug supply chain are complicating the pharma company outlook as well. Manufacturers have been dealing, successfully in most cases, with maintaining safe operations and availability of inputs, especially from India and China. But problems remain further downstream in the supply chain, including airline-dependent logistics and shortages at the pharmacy and patient level resulting from stockpiling and hoarding (see Figure 3).

Implications for the industry

Lewis expects the pharma industry, and the rest of the global economy, to endure a slow recovery, with a vaccine not broadly available before mid-2021 and a return to “normalcy” in 2022 at the earliest. The possibility of follow-on waves of virus outbreak pushing back the recovery means that companies face a substantial amount of uncertainty. As a result, he advises companies to continuously review plans and forecasts as new information comes in.

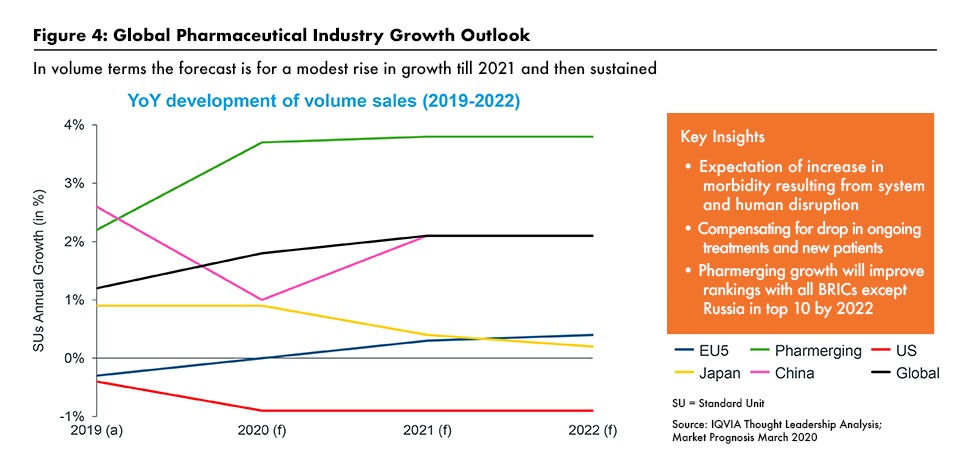

IQVIA’s current outlook for the pharmaceutical industry is for modest revenue growth in developed markets as the implications of the pandemic really take hold (see Figure 4). Pricing pressures will grow, especially in the US, as health systems, commercial insurers and the government look for ways to offset the extreme cost burden they have borne during the pandemic. Buyer pressures for discounts and rebates has been pushing down the growth in net prices received in the US for several years. A significant exception may be for US generic drug prices, which appear to have stabilized recently after a period of intense downward pressure.

The industry will face other headwinds as well in the US and Europe. Sales could be impacted as the industry reduces its dependence on face-to-face visits for provider-sales rep interactions, and detailing activity may lag the overall recovery during the transition to more digital channels. The industry will feel the delays in new drug launches as well.

The pharmerging markets are likely to enjoy somewhat more robust growth in the next two years. Pharmerging countries, including India, Brazil, and Russia, are likely to achieve growth rates that are even higher than those experienced in recent years, thanks in part to accelerating growth in specialty segments such as oncology.

Supply chains are likely to undergo significant restructuring, but the process is likely to set off national debates over the trade-offs involved. Most notably, Lewis points out, repatriating more drug manufacturing from offshore suppliers will increase security of supply and product quality but is likely to require higher prices to offset the higher costs.

Ultimately, pharmaceutical companies are likely to see their margins squeezed between price pressures on the top line and the higher costs of supply-chain restructuring and new channels for interacting with providers and patients. Even broader changes are possible as government and citizen views of health care as a “public good” evolve. Healthcare providers and pharma companies will need to work even harder to manage costs as they broaden accessibility to care and medicines.

Lewis ended by stating that despite the unprecedented challenges, there is a great opportunity for the pharma industry to capitalize on the huge amount of goodwill generated among all stakeholders by supporting the healthcare system through a period of significant stress, and investing heavily in treatments and new vaccines. Enhanced partnerships with customers to return healthcare to a ‘new’ normal and provide enhanced levels of service and support should ensure that the pharma industry is seen as an effective and valued partner in navigating the many challenges and opportunities which lie ahead.

Market re-assessment coming this fall

Lewis and his IQVIA colleagues are closely monitoring the constantly changing situation relating to the pandemic and its implications for countries, economies, and the pharmaceutical industry. He will be providing the latest market information and assessment for IQVIA’s outlook for the global pharmaceutical industry for the DCAT audience in a webinar in late October. Further information, including how to register, will be forthcoming on the DCAT website.

Note: DCAT would like to thank our sponsors, Thermo Fisher Scientific and West Pharmaceutical Services, for their support for the June 30, 2020 DCAT webinar, Pharma Industry Outlook, which served as the basis for this article.

| |

|