Oncology Drug Market: The Ups and Downs

ASCO’s Annual Meeting, held this week in Chicago, is when bio/pharma companies highlight the most promising in their cancer drug pipelines and portfolios. What is the outlook for the global oncology drug market?

By Patricia Van Arnum, Editorial Director, DCAT, pvanarnum@dcat.org

Oncology drug market: a snapshot view

The annual meeting of the American Society of Clinical Oncology (ASCO), concluded this week (May 29 to June 2, 2026), is a time when bio/pharma companies highlight the latest developments in their oncology drug pipelines and commercial portfolios. Oncology represents the largest therapeutic sector in the global bio/pharmaceutical industry on a value basis and is continually one of the highest growth areas. What is the outlook for the global oncology drug market, and what are the greatest growth prospects?

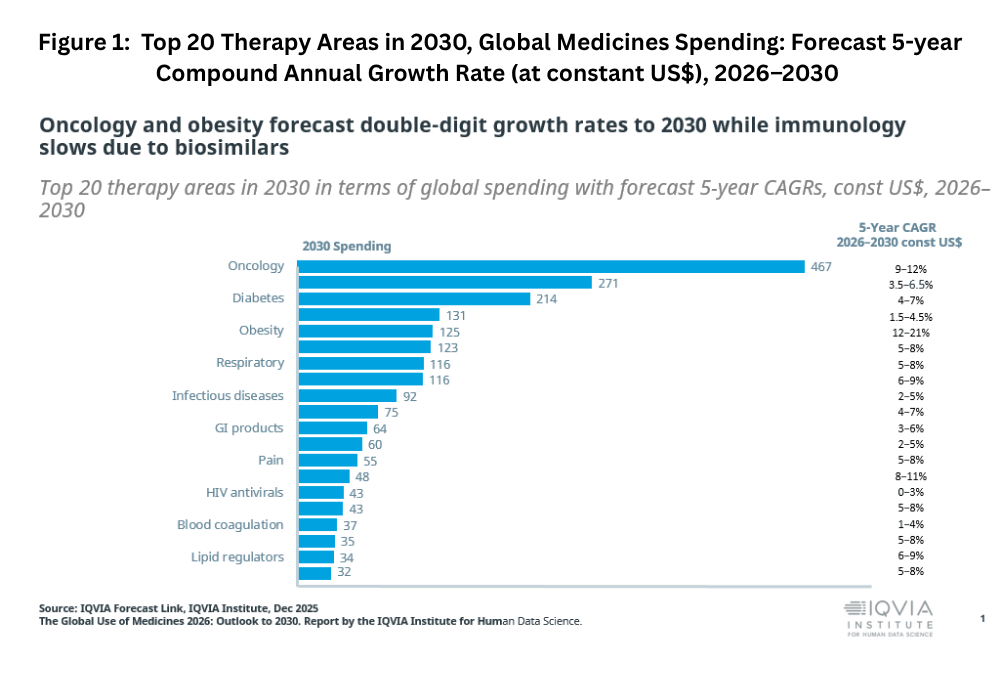

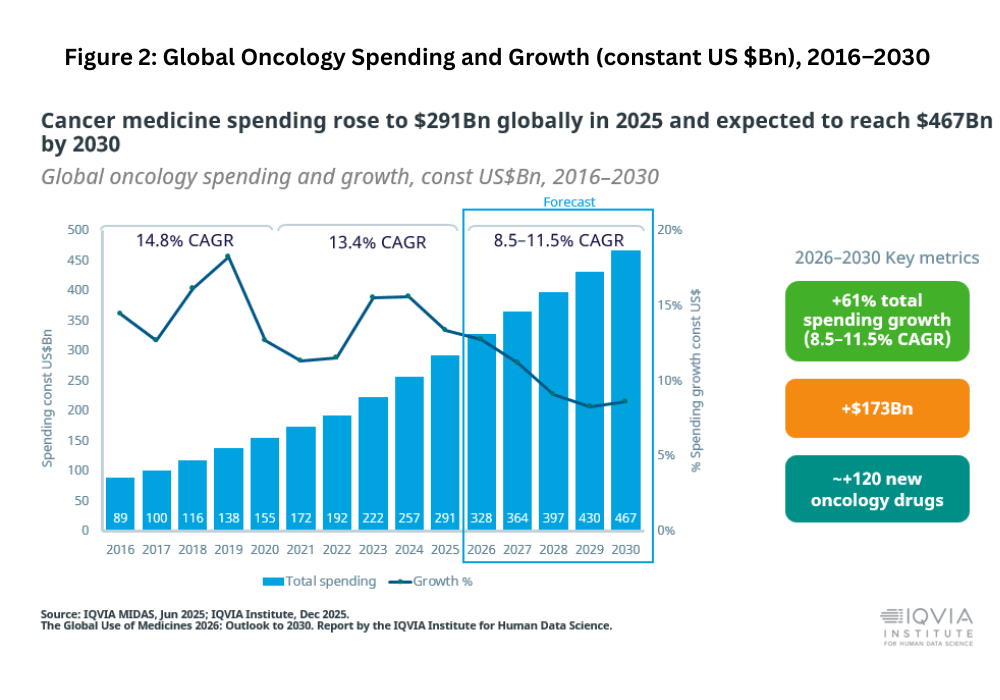

Global spending on cancer medicines, not including additional medical costs or supportive care medicines, rose to $291 billion globally in 2025 and is expected to reach $467 billion by 2030, representing a compound annual growth rate (CAGR) of approximately 9-12%, according to a recent analysis, Global Medicines Use Trends 2026 by the IQVIA Institute for Human Data Science. Oncology continues to be the largest therapeutic sector on a value basis followed by immunology, diabetes, cardiovascular, and obesity (see Figure 1 below) and whose CAGR is only surpassed by the obesity drug market. In terms of product innovation globally, there have been 235 oncology drugs launched in the past decade, 143 in the past five years, and more than 120 are expected in the next five years.

With the strong growth, there are some headwinds. Growth in cancer medicines spending averaged 13.4% annually 2021–2025, including slower growth in 2021 and 2022 as countries continued to recover from the COVID-19 pandemic. Growth is expected to slow beginning in 2027 as a number of therapies begin to face generic and biosimilar competition (see Figure 2).

On the small-molecule side, Pfizer’s Ibrance (palbociclib) for treating breast cancer, Pfizer’s/Astella’s Xtandi (enzalutamide) for treating several types of advanced prostate cancer, and AstraZeneca’s/Merck & Co.’s Lynparza (olaparib) for treating various tumors will lose patent exclusivity in 2027. On the biologics side, the PD-1 inhibitors, Merck & Co.’s Keytruda (pembrolizumab) and Bristol-Myers Squibb’s Opdivo (nivolumab), which combined accounted for 10% of global oncology spending in 2025, are expected to face biosimilar competition starting in 2028, with much of this impact on growth in 2029. This lower growth as the result of losses of exclusivity will be offset by continued uptake of novel modalities, including antibody drug conjugates (ADCs), bispecific antibodies, and cell and gene therapies, which are expected to account for nearly 20% of oncology medicines spending in 2030, up from 10% in 2025 and 4% in 2020, according to the IQVIA Institute analysis.

Oncology drug R&D: the continued rise of novel modalities

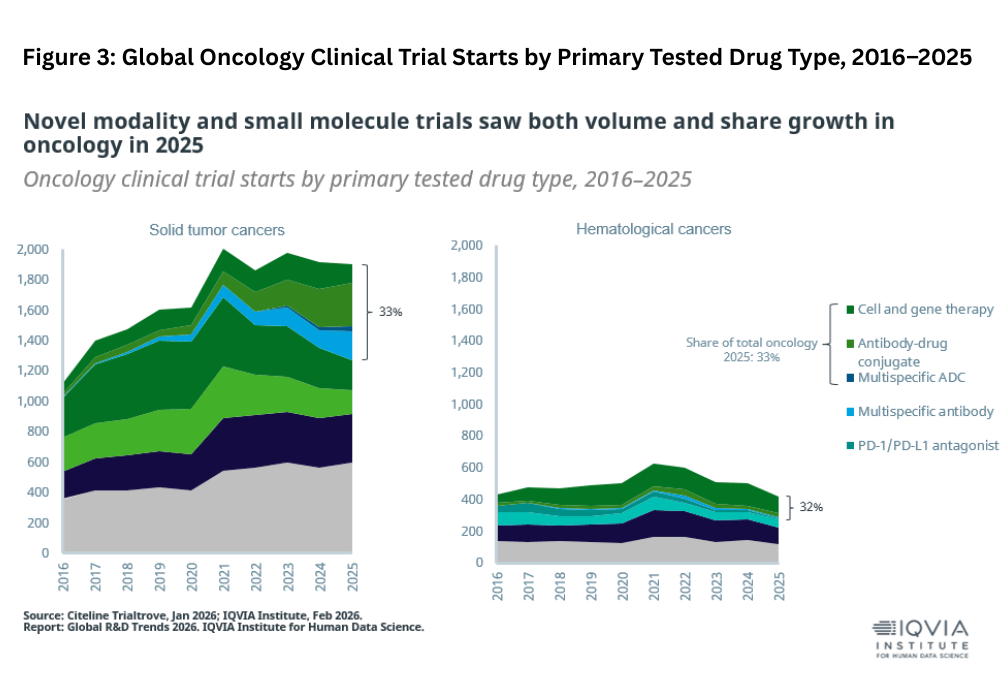

This increased market penetration will be reflective of the considerable growth for new modalities within oncology R&D, according to a further analysis by the IQVIA Institute, Global R&D Trends in 2026. In 2025, novel modalities, including cell and gene therapies, ADCs, bispecific and other multispecific antibodies collectively accounted for 33% of oncology clinical trials, triple the 2016 figure of 11%. In solid tumors, multispecific antibodies (including bispecifics) accounted for 10% of clinical trial starts in 2025 while monospecific ADCs accounted for 15% and cell and gene therapies accounted for 6%; a newly emerging category of multispecific (generally bispecific) ADCs accounted for 2%. Despite the small 2025 share of multispecific ADCs among solid tumor trials, this category is notable for its accelerating growth, increasing from 3 to 33 clinical trial starts in the last five years, according to the IQVIA Institute analysis (see Figure 3 below).

In oncology as a whole, PD-1/L1 antagonists and kinase inhibitors still account for high, but declining shares of clinical trial starts, with each category falling from 19% in 2016 to 9% in 2025, according to the IQVIA Institute analysis. Beyond novel modalities, solid tumor trials were also notable for large increase in volume and share of small-molecule trials, up from 415 in 2020 to 600 in 2025, an increase of 45%.

The rising role of China-based innovation

Another important trend overall for the bio/pharmaceutical market and for oncology drugs specifically is the rising role of China in R&D as measured in both clinical trial starts and deal-making with international partners.

Trial starts from China-headquartered sponsors have mainly been driven by domestic-only trials, referring to those that were exclusively conducted in China, which account for between 75% and 88% of China-headquartered sponsor trials. China-headquartered companies accounted for 39% of global oncology trial starts, according to the IQVIA Institute analysis.

This high level of domestic trial activity has also resulted in China becoming the top location globally for industry sponsored single-country trials by Emerging Biopharma companies. In addition, licensing, merger and acquisition deals between China-headquartered biopharma companies and international companies overall (not specific to oncology) surged to an all-time high in 2025, with almost half of these deals involving a US partner, according to the IQVIA Institute analysis. The overall number of international deals for China-based companies surged in 2025, with 94 M&A or licensing deals, up from 71 in 2024, and with the largest increase from North American companies, predominately the US, followed by European companies.