Inside the Market for High-Potency APIs

What’s behind continuing investment in manufacturing capabilities for high-potency APIs (HPAPIs)? The potential in innovator drugs is a driving factor, but the supply opportunities for generic drugs with HPAPIs also comes into play.

High-potency active pharmaceutical ingredients (HPAPIs) continue to be an area of interest to the pharmaceutical manufacturing sector. Some market estimates project that the global HPAPI market could reach $26 billion by 2023 (1). Behind these opportunities, however, are questions related to the degree to which this segment represents a differentiated opportunity or strategic portfolio play, and whether this segment is in any way distinct or insulated from overall market trends and challenges. Deeper analysis indicates that, in addition to services for innovator pharmaceutical companies, the generics side of the industry will drive meaningful growth in the HPAPI market. Also, dozens of manufacturers are investing in the space, not just the largest players, suggesting that emerging firms see an opportunity for accelerated growth from new product introductions and will, accordingly, compete aggressively. Consequently, rather than representing a truly specialized sector, trends in high-potency manufacturing worldwide appear to be following the course of the pharmaceutical market overall.

|

|

Brandon Boyd |

Inside the HPAPI market

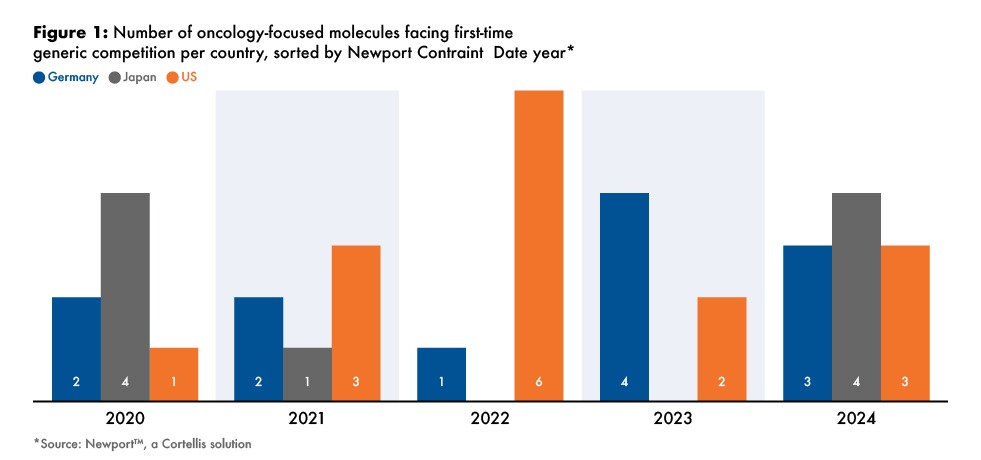

The HPAPI market covers a wide range of product types across several therapeutic areas although oncology-focused medicines continue to lead in terms of innovative pipeline candidates and upcoming generic entries, which reflects broader pharmaceutical industry trends. Consistent with this dynamic, at least 27 high-potency cancer-fighting molecules, generating over $26 billion (2) annually in brand value, could face loss of exclusivity (LOE) between 2020 and 2024. Almost all of these molecules are protein kinase inhibitors (e.g., dasatinib, gefitinib, olaparib). LOE timing here is estimated using Newport Constraint Date, a proprietary Cortellis analytic of Clarivate Analytics, which considers patents and exclusivities at the country/territory level. Figure 1 summarizes the situation in three of the largest pharmaceutical markets—the US, Japan, and Germany. Importantly, nine of these 27 HPAPI products face potential LOE in more than one major market during this five-year horizon (including countries not sampled here), highlighting the general attractiveness of these opportunities. This collection of 27 products, therefore, offers a useful reference point for reviewing opportunities overall in high-potency active ingredients and exploring how HPAPI products fit into portfolio strategies across various regions and company types.

As previously outlined, these high-potency products are attracting interest from many API companies. About half of the compounds are expected to face the highest levels of competition, meaning excessive supply across regulated markets, as shown in Table 1. This projection is based on intelligence also from Newport, a Cortellis solution, which ranks API availability in regulated and less regulated jurisdictions on a five-point scale. Only two of the 27 molecules have no confirmed sources of commercially available APIs at present. Not surprisingly, raw material availability is highly correlated with innovator brand revenues; the higher the original product sales, the more manufacturers are developing APIs. Consequently, suppliers should expect these markets to be very price competitive like most other molecules, even in highly regulated jurisdictions, and not necessarily assume that high brand value will translate to relatively high, sustainable generic value.

| Table 1: 27 High-potency Active Pharmaceutical Ingredients (HPAPIs) Facing Loss of Exclusivity in Three Major Markets (the US, Germany and Japan), 2020-2024, Grouped by Active Pharmaceutical Ingredient (API) Supply Availability Rating |

|||

|

API Availability Rating (1 = least available, 5= most available) |

Number of Molecules |

Average Number of Active US Drug Master Files per Molecule |

Estimated 2019 Brand Drug Sales |

| 5 | 13 | 11 | $21 Billion |

| 4 | 3 | 5 | $1 Billion |

| 3 | 3 | 2 | $2 Billion |

| 2 | 6 | 2 | $2 Billion |

| 1 | 2 | 0 | $70 Million |

|

Source: Newport, a Cortellis solution; Cortellis Competitive Intelligence |

|||

Supplier base for generics with HPAPIs

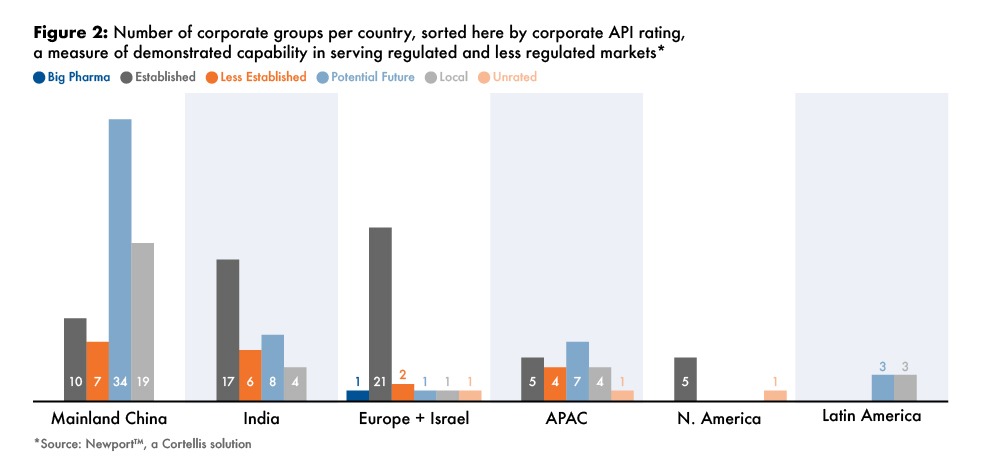

Drilling into the manufacturers associated with these HPAPIs reveals a wide array of firms in terms of geographic footprint and level of demonstrated capabilities. About 165 separate corporate groups are already involved in development or commercial sale of these 27 molecules, excluding those dedicated to making the original branded versions. These API producers are headquartered in 24 different countries/territories, though most are based in either India or mainland China (see Figure 2). Again, this is in line with conditions in the broader market. The largest corporations, about one-fifth of the total, have two or more sites associated with HPAPI production although not necessarily actively manufacturing these specific compounds. Generalizations aside, important distinctions are apparent when comparing the experience level of individual manufacturers, evaluated here according to Newport Corporate API Ratings, a measure of a supplier’s track record serving various markets. Less than half of the companies in the cohort (78 companies) have a track record of sustained activity in regulated markets such as the US, and could thus be expected to fully realize the potential of these upcoming LOE opportunities.

In contrast, the other half of the company cohort appear to have motivations other than the upcoming LOEs in major markets. For example, while China boasts 70 corporate groups linked to just this subset of HPAPIs, 75% have little-to-no experience serving regulated markets. Indeed, judging by a lack of regulatory filings (drug master files or certificates of suitability) from these firms, their strategy appears to be to capitalize on the growing domestic opportunity. This is not surprising, given the emphasis the Chinese government has placed on expanding the capabilities of the local pharmaceutical industry, especially in therapy areas such as oncology. The landscape is similar in Latin America, and to some extent, Asia-Pacific, where traditionally local manufacturers and smaller-scale exporters meet most of the need in the domestic or regional market. In short, investment in HPAPI products by these companies is consistent with local conditions and not a sign of transformational global ambitions driven by a special set of new opportunities emerging in major markets.

Turning back to the more regulated markets, and the more experienced players serving them, it’s worth further examining how high-potency products fit into the growth story, given the attention the category has received lately. As the figures previously presented show, this is not a consolidated market segment. To underscore this point, out of the 27 compounds highlighted here, these more experienced players are associated with an average of four molecules. In fact, most are pursuing three or less. Only seven corporate groups (five in India, one in Israel, one in China) are active in 10 or more of these compounds. None are known today to be pursuing all 27; the highest number is 21. In other words, it is not apparent that companies are shifting resources toward more high-potency products and away from other potential product opportunities. What, then, is this dynamic in the context of the well-documented portfolio play expansions previously cited?

Key takeaways

Looking just at this subset of products makes it difficult to draw definitive conclusions about a given firm’s portfolio strategy. That said, these data at least suggest that the high-potency nature of these products was not the primary criterion for selection by many, if not all, manufacturers. In other words, it does not seem to be the case that investments in HPAPI production capabilities necessarily derives from a deliberate platform strategy, or leads to a broad portfolio of high-potency products. Other forces, including resource constraints and global trends, are still significant factors. To the degree that individual firms view high-potency products as strategic growth drivers, these manufacturers are still being as selective in evaluation and development of these products as they are with any other new product opportunity.

New product introductions are a core growth driver for the generic API industry, and many of the upcoming opportunities are oncology-focused, high-potency compounds. Accordingly, many manufacturers—across many territories and levels of experience—have been making investments in HPAPI capabilities. This level of manufacturing activity seems similar to most other categories of products. Thus, companies should anticipate similarly high levels of competition as product markets develop. To the degree that these molecules accelerate growth for manufacturers, this will result from the unique characteristics of the individual product markets, rather than from the high-potency nature of the product. In sum, rather than representing a well-differentiated, more insulated market segment, trends in HPAPIs are still aligned closely with the underlying dynamics of the pharmaceutical industry overall, and investments in the space should be viewed as requisite steps to keep pace with the market.

References

1. High Potency APIs /HPAPI Market by Type (Innovative, Generic), Synthesis (Synthetic, Biotech, mAb, Vaccines, Recombinant Proteins), Manufacturer (Captive and Merchant), Therapy (Oncology, Glaucoma, Hormonal Imbalance) Global Forecasts to 2023, Research and Markets (April 2018).

2. Cortellis Competitive Intelligence, Clarivate Analytics.