Industry Roundtable: Small-Molecule APIs: What’s in Store for 2026?

What are the pressing issues shaping the market for fine chemicals and pharma ingredients in 2026—the challenges and the opportunities? Senior executives from CDMOs share their perspectives.

By Patricia Van Arnum, Editorial Director, DCAT, pvanarnum@dcat.org

What’s in store for 2026?

DCAT Value Chain Insights tapped into the expertise of senior executives from CDMOs of small-molecule active pharmaceutical ingredients (APIs) to gain their views on the key issues shaping the market for fine chemicals and pharma ingredients in 2026. Topping the list is the dynamic tariff/trade situation and its impact on manufacturing strategies, supply planning, and “make-versus-buy decisions.” At the same time, the pipelines and commercial portfolios of bio/pharma companies continue to provide opportunity for CDMOs in meeting demand for more complex drugs, including new modalities, as advanced and emerging technologies, including artificial intelligence (AI) and other forms of digitalization, become increasingly important in building capabilities in manufacturing and supply chain management.

Participating in the roundtable were: Julian Piallat, Supply Chain Director, Axplora; Jan Vertommen, PhD, Vice President, Head of Commercial Development, Advanced Synthesis, Lonza; Krishna Kanumuri, Managing Director and CEO of Sai Life Sciences; and Joerg Ahlgrimm, CEO of SK pharmteco.

Q: What do you see as the three top issues driving the CDMO market for fine chemicals and pharma ingredients in 2026?

Ahlgrimm (SK pharmteco): In 2026, the CDMO market for fine chemicals and pharma ingredients has successfully moved past the ‘post-COVID hangover,’ entering a phase of renewed investment and strategic clarity. However, this growth is being shaped by three pivotal forces that determine which players will thrive in an increasingly competitive landscape.

First: Geopolitical regionalization and the ‘US requirement.’ The geopolitical environment has made supply-chain resilience and regionalization essential. For innovative companies, manufacturing within the United States has shifted from a preference to a necessity for securing reliable market access. This change benefits organizations with strong domestic capacity as sponsors increasingly favor partners who can shield their programs from global trade instability and fragmented logistics.

Second: The battle against ‘internal build.’ The main competitor for a CDMO in 2026 is often not another service provider but a client’s own desire to develop internal capabilities. To remain the ‘first-best’ strategic choice rather than a fallback option, CDMOs must shift from transactional vendor relationships to genuine partnerships. Success now relies on a CDMO’s ability to deliver high-level value through operational excellence and performance that justify outsourcing rather than the perceived control of in-house manufacturing.

Third: Structural market bipolarity: consolidation vs. contraction. The industry is experiencing a significant split in market structure. On one side, aggressive consolidation, such as the Novo Holdings–Catalent deal, is changing the traditional competitive landscape. On the other hand, the advanced therapy sector is undergoing a necessary contraction. As cell and gene therapies approach commercial maturity, the industry is seeing facility closures and layoffs, requiring remaining CDMOs to show strong resilience and long-term viability.

Vertommen (Lonza): In 2026, the CDMO market will be driven by rising demand for complex modalities, such as highly potent APIs (HPAPIs), as well as the need for speed and flexibility to accelerate and scale the development of breakthrough therapies. We expect demand to be strong, and CDMO capacity will be limited, especially for the development and manufacturing of innovative payload–linkers for antibody drug conjugates (ADCs). Additionally, adapting to increasingly diverse and evolving local regulatory requirements will be essential for success.

These trends are driven by a surge in innovation targeting areas such as oncology, central nervous system disorders, and endocrine conditions, including diabetes and weight loss. Some of the innovative drugs are expected to need large volumes of APIs, often coupled with the use of bioenhancement technologies such as spray drying of these APIs. This may require additional capacity investments to meet demand. Furthermore, technological innovations, especially in AI, will play a key role in reshaping investment strategies, with speed and efficiency remaining top priorities for biopharma companies.

Piallat (Axplora): In 2026, three forces will shape the CDMO market for fine chemicals and pharma ingredients.

First, product and process complexity will continue to increase. More programs require high containment, specialized equipment, and advanced expertise, particularly for highly potent compounds and advanced therapies. At the same time, small molecules will remain the backbone of the pharmaceutical industry, representing the majority of medicines produced and used globally. CDMOs must therefore support both innovation and continuity, scaling complex programs while protecting reliable small-molecule supply.

Second, regulatory and quality expectations will keep intensifying. Global standards from EMA [European Medicines Agency], FDA [US Food and Drug Administration], and other agencies continue to evolve, requiring strong quality systems, compliant infrastructure, and higher levels of traceability. This increases the investment needed to maintain inspection readiness, validate processes, and deliver consistent performance across both traditional and more complex product types.

Third, supply-chain resilience will remain a major differentiator. Volatility in raw materials, ongoing geopolitical uncertainty, and logistical disruption all continue to affect lead times and continuity. CDMOs will need to diversify sourcing strategies, reduce dependency on single points of failure, and build flexibility into planning and inventory management. This is critical not only for advanced therapies, but also for the small-molecule supply chains that underpin global healthcare.

Overall, customers are increasingly looking for CDMO partners that can combine technical capability with operational reliability and that can support long-term programs with confidence and transparency

Kanumuri (Sai Life Sciences): The first is a clear shift from cost optimization to supply-chain resilience. After several years of disruption, innovator companies are reassessing how and where they source critical ingredients. Reliability, regulatory credibility, and continuity of supply now weigh as heavily as price. This is favoring CDMOs with long inspection histories, strong quality cultures, backward-integrated capabilities, and the ability to move seamlessly from clinical to commercial production without introducing new compliance risk.

The second is the growing complexity of R&D portfolios. We are seeing more high-potency compounds, intricate chemistries, and small-molecule programs supporting emerging therapeutic modalities. That complexity is pushing companies away from fragmented outsourcing toward deeper, strategic partnerships with CDMOs that can integrate development and manufacturing, maintain tighter process control, and safeguard intellectual property.

The third is the premium placed on speed to clinic and speed to market. For innovators managing competitive pipelines and finite capital, time has become a strategic variable. CDMOs are increasingly expected to help shape programs early—optimizing synthetic routes, designing regulatory-ready processes, and aligning development choices with eventual commercial and market-specific requirements. That early integration, particularly for US and European filings, reduces late-stage surprises and materially improves the likelihood of first-pass regulatory success.

Q: Evolving US tariff/trade policy was a key issue in 2025 and continues to be in 2026. From a CDMO view, what are the primary issues of particular importance, including points of policy clarification needed by the industry in responding to tariffs? What has been the impact to date in supply planning—from a CDMO perspective in contract fulfillment as well as sourcing activities?

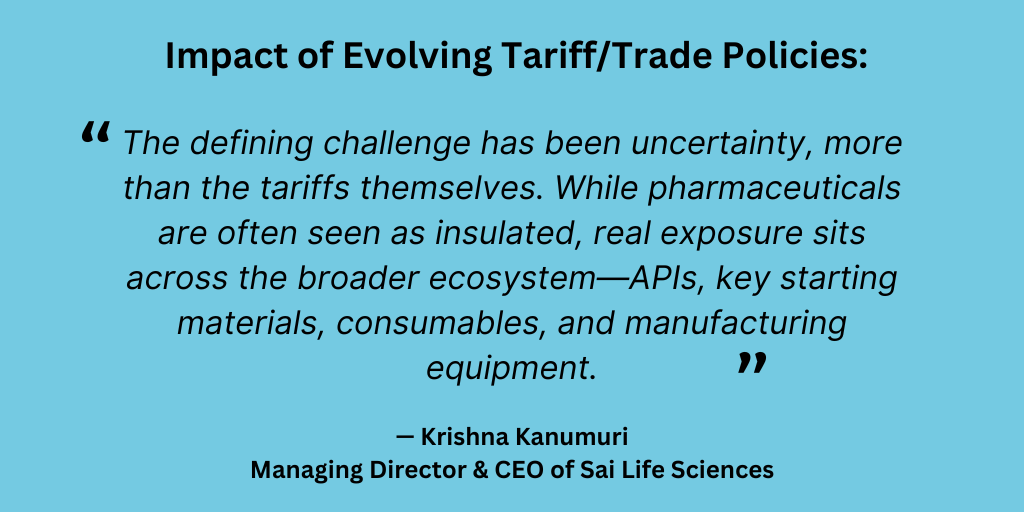

Kanumuri (Sai Life Sciences): The defining challenge has been uncertainty, more than the tariffs themselves. While pharmaceuticals are often seen as insulated, real exposure sits across the broader ecosystem—APIs, key starting materials, consumables, and manufacturing equipment. What the industry needs is clarity: what is in scope, how country of origin will be determined across multi-country supply chains, whether different tariff regimes can stack, how durable exclusions will be, and how US manufacturing is defined when production is carried out through CDMOs. These points materially influence long-term supply-chain design and investment decisions.

In response, companies have taken a more cautious approach to planning. US inventories are higher, procurement is being pulled forward, and additional sites are being qualified earlier to preserve flexibility. Contracts increasingly address tariff treatment explicitly, and working-capital needs have risen as buffer stocks grow. The industry is adapting pragmatically, but greater policy stability would enable more confident long-term planning.

Piallat (Axplora): From a CDMO perspective, tariffs remain a significant challenge, both because of cost impact and because of uncertainty. The most important issue is the lack of clarity around scope and exemptions, including which products are covered, how country-of-origin rules are applied, and how complex multi-step supply chains are treated. This uncertainty makes it difficult to define accurate cost forecasts, sourcing strategies, and investment plans. Tariffs also increase the burden of trade compliance and can trigger additional regulatory complexity. In some cases, a change in sourcing or manufacturing location can require requalification activities, updated documentation, and additional GMP validation work. From a commercial standpoint, fixed-price contracts are particularly exposed. Tariff-related cost increases can erode margins if they cannot be passed through, potentially forcing contract renegotiation and creating risk for both CDMOs and customers.

In supply planning, tariffs have contributed to longer lead times and higher input costs, including raw materials and equipment. This can drive the need for higher safety stock and additional working capital, reducing agility and increasing warehousing costs. These effects are especially important for small molecules, where supply continuity and volume requirements are high, and where disruption can have wide downstream impact. While diversification is a priority, many supply chains remain structurally dependent on China for starting materials. Alternatives are limited in the short term, and qualification timelines can be long, particularly for regulated products. Overall, tariffs are accelerating the need for more resilient and regionally balanced supply models, but the transition requires time, clarity, and investment.

Ahlgrimm (SK pharmteco): Recent proposed punitive US trade measures include very high tariffs on certain imported branded or patented pharmaceuticals (up to 100%), with lower caps for some EU and Japanese products and exemptions for generics. Separately, tariffs on Chinese-origin products typically start around 10% and can exceed 30%, affecting selected APIs, intermediates, and manufacturing inputs. For CDMOs, this creates a patchwork where APIs may be treated differently from finished dose forms. Additionally, origin matters (China vs. EU vs. Japan vs. UK/Switzerland, etc.), forcing complex cost modeling at the project level. Without clear, stable harmonized system-code guidance, it’s difficult to lock in pricing and long-term supply agreements.

Tariffs are intentionally used to direct investment into US based manufacturing for high-value pharmaceuticals and inputs. CDMOs need clear criteria for what constitutes enough US investment to avoid tariffs or secure preferential treatment. This influences long-term site planning and capital decisions. From a CDMO perspective, the most important clarifications are:

• Clear, stable lists for APIs, key starting materials, intermediates, biologics inputs, and equipment;

• Treatment of clinical and R&D materials versus commercial volumes;

• Rules of origin for multi-country value chains and what qualifies as substantial transformation; and

• Clear guidance on exemptions (e.g., critical shortages, essential medicines lists, orphan/rare disease products).

Vertommen (Lonza): In today’s unpredictable geopolitical and economic climate, CDMOs need a well-diversified global presence, including significant capacity in the US, and a resilient supply chain strategy grounded in long-term planning, robust risk management, and operational flexibility. This approach allows companies to better support customers facing regulatory requirements, shipping delays, and geopolitical uncertainties while also helping to mitigate the effects of shifting trade policies when necessary.

To overcome challenges in supply planning, offering end-to-end solutions from early development through commercial manufacturing helps mitigate disruptions for drug developers. Additionally, adopting new technologies that enable real-time analysis can enhance efficiency throughout the planning process.

Q: From a macro view, what other external factors, such as legislative or regulatory changes globally, will be impactful to the fine chemicals and pharma ingredients market in 2026 and why?

Ahlgrimm (SK pharmteco): From a macro perspective, several global forces beyond trade policy will shape the fine chemicals and pharma ingredients market in 2026. First, cost and pricing pressure will continue to intensify. Drug pricing and reimbursement dynamics in the United States and Europe are pushing pharmaceutical companies to scrutinize supply chains more closely. This increases the importance of operational efficiency, automation, and scale for ingredient manufacturers.

Second, supply chain resilience has become a strategic priority. Governments in the United States and Europe are increasingly focused on securing access to critical medicines and ingredients. This is driving incentives for domestic and regional manufacturing, greater expectations around redundancy, and stronger requirements for supply continuity and transparency. Third, regulatory standards are rising globally. Environmental, safety, and quality expectations are tightening across major markets. Compliance will require sustained investment, but it will also favor manufacturers with strong quality systems, proven regulatory track records, and the ability to support advanced and complex therapies.

Fourth, Europe is advancing toward a more unified pharmaceutical and chemicals framework. New legislation is expected to simplify approval processes while holding companies more accountable for preventing shortages and maintaining a reliable supply. This emphasizes the strategic importance of audit-ready, regionally based manufacturing capacity. Finally, Asia remains a vital part of the global ecosystem, but its dynamics are changing. Regulatory oversight is increasing, and customers are more focused on diversification and risk management. This supports a more balanced global footprint and enhances the role of trusted partners who provide consistent quality and compliance. Taken together, these trends point to a market that increasingly rewards scale, reliability, regulatory excellence, and proximity to customers and patients.

Piallat (Axplora): In 2026, several external factors will continue to reshape the fine chemicals and pharma ingredients market.

Geopolitics and national industrial policy are driving a stronger focus on supply security. Initiatives that support onshoring, restrict exports, or reduce reliance on at-risk regions are fragmenting global supply chains. While this can improve resilience, it also creates pressure for duplicated investment and can increase overall costs across the industry. At the same time, regulatory expectations are expanding and increasingly include upstream materials and supplier transparency. This adds complexity and cost and may place weaker or less mature producers under pressure, particularly those unable to invest in the systems and infrastructure needed to meet rising standards.

Sustainability and ESG expectations are also becoming more influential in decision making. Customers and regulators increasingly expect measurable progress on greener chemistry, solvent reduction, recycling, and energy efficiency. These requirements may accelerate the shutdown of legacy facilities that cannot adapt or cannot access the capital required for modernization.

Finally, market volatility remains a reality, driven in part by clinical attrition and funding constraints in biotech. This increases demand uncertainty and reinforces the need for CDMOs to maintain flexible, modular capacity. However, these expectations come at a time when capital costs remain high, and investment conditions are tighter.

In this environment, the CDMOs best positioned for success will be those that combine resilient supply networks and strong compliance capabilities, while continuing to protect small molecule capacity, which remains essential to global healthcare.

Vertommen (Lonza): Although legislative and regulatory challenges have long been a part of the pharmaceutical industry, it is vital to have a dedicated team actively monitoring trends and developments. Proactive planning is essential to minimize risks during product development. In the short term, we can expect an increased focus on more sustainable operations, a more modernized review processes utilizing AI and digital tools, and a greater emphasis on strengthening supply chain resilience.

Kanumuri (Sai Life Sciences): Trade policy is only one part of the picture. A second, equally powerful force is regulatory evolution. Across the United States, Europe, and Asia, expectations around data integrity, traceability, and digital documentation continue to rise. For ingredient manufacturers, this means sustained investment in systems, automation, and quality infrastructure. At the same time, environmental regulation, particularly in Europe and parts of Asia, is becoming more exacting, raising the cost of traditional chemical manufacturing and accelerating the transition toward greener processes and more resource-efficient technologies.

There is also a structural shift driven by governments themselves. Incentives for domestic or ‘trusted partner’ manufacturing of critical medicines are influencing where future capacity is located. Alongside this, drug-pricing and reimbursement reforms in major markets are tightening margins, which inevitably sharpens the focus on operational efficiency and cost-effective sourcing. Overlaying all of this are geopolitical tensions and currency volatility, which add complexity to investment and supply-chain decisions that already span many years.

Q: Artificial intelligence (AI) and other forms of digitalization are important tools in global supply chains as well in manufacturing. What do you see as key or emerging technology trends in 2026 in these areas?

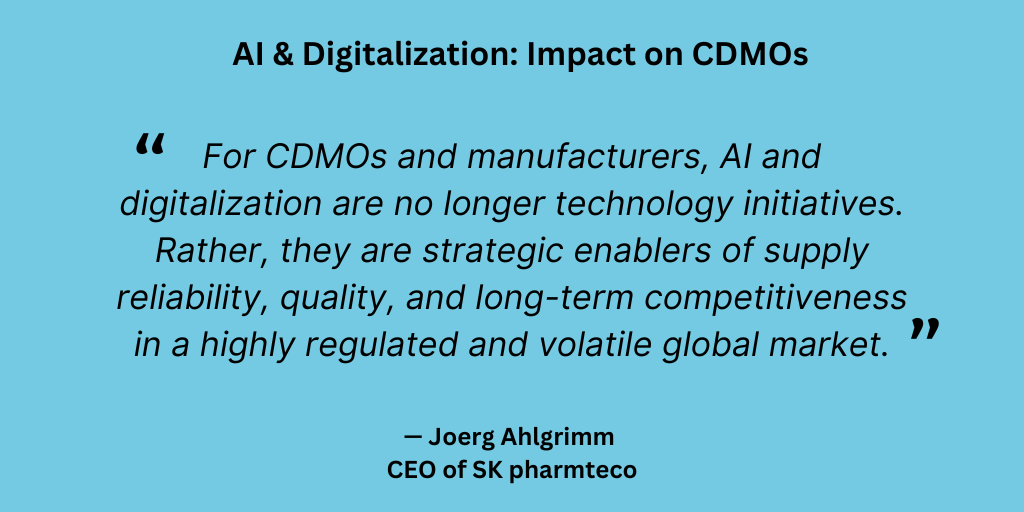

Ahlgrimm (SK pharmteco): For CDMOs and manufacturers, AI and digitalization are no longer technology initiatives. Rather, they are strategic enablers of supply reliability, quality, and long-term competitiveness in a highly regulated and volatile global market. 2026 technology trends in manufacturing include:

• Generative, agentic and autonomous AI technologies are moving into the core of operations. Companies are scaling trusted, validated AI technologies to improve yields, reduce risk, and strengthen execution across their manufacturing networks.

• Digital foundations for growth. Investing in modern platforms enables faster tech transfer, multi-site harmonization, and resilient global supply, positioning companies for future expansion.

• Increased cyber security investments: Cybersecurity and data integrity are now foundational to protect IP [intellectual property], ensure compliance, and maintain partner and regulator confidence.

• Automation drives efficiency with resilience. Automation and AI drive productivity and cost discipline while supporting consistent, right-first-time manufacturing.

• AI and machine learning are enabling predictive operations. Digital intelligence enables earlier visibility into quality, process, and supply risks, allowing issues to be addressed before they impact customers or patients.

Vertommen (Lonza): As the industry evolves rapidly, both investors and innovators will increasingly seek partners capable of accelerating development and scaling up with precision and reliability. AI and machine learning (ML) will remain central to manufacturing by optimizing production processes, ensuring quality control, and predicting needs in equipment maintenance. Through real-time analysis of manufacturing data, AI can detect and correct process deviations, which maximizes yield and minimizes waste. Predictive maintenance algorithms help anticipate equipment failures, reducing downtime, and supporting a resilient supply chain.

Today, we’re implementing ML algorithms and AI to navigate the complexity and speed requirements of developing and manufacturing novel treatments and accelerate the synthesis of APIs. Our AI-enabled Route Scouting Service, for example, combines extensive, proprietary commercial supply chain data in the industry-leading computer-aided synthesis planning technology. As we look ahead, predictive modelling could be expanded to optimize synthesis routes, not only for efficiency and cost, but for plant fit, utilizing existing assets and equipment to the fullest. Additionally, AI-driven retrosynthetic analysis could integrate real-time supply chain and production data to dynamically adjust routes based on current plant capacities, inventories, and operational constraints.

Piallat (Axplora): By 2026, AI and digitalization will increasingly become core enablers of performance and resilience for CDMOs. In supply chain operations, AI-driven planning tools will continue to develop, enabling more scenario-based forecasting and better anticipation of disruption. These models can integrate clinical demand signals, regulatory timelines, geopolitical risk, and supplier reliability to support stronger decision making and reduce last-minute changes. In process development and scale-up, AI can accelerate optimization by supporting smarter experimentation, faster parameter selection, and improved yields. This reduces time and waste, which is valuable across both complex programs and high-volume small molecule manufacturing.

Quality systems are also evolving through better data analytics and real-time monitoring. The next stage is predictive quality assurance, where deviations can be reduced, investigations can be faster, and batch release can be more efficient, while maintaining compliance. Digital traceability is becoming increasingly important, both for transparency and risk management. Enhanced tracking of materials and supplier risk scoring will help CDMOs respond to customer expectations linked to tariffs, geopolitics, and ESG requirements. Automation will also expand, including the use of robotics and semi-autonomous systems in production, warehouses, and laboratories. While investment can be significant, these technologies help address labor constraints, improve consistency, and reduce operational risk.

Overall, AI and digitalization will increasingly differentiate CDMOs by strengthening reliability, improving efficiency, and supporting resilient supply chains across both emerging therapies and the small molecule backbone of pharma.

Kanumuri (Sai Life Sciences): What is becoming clear is that the most valuable applications of AI will be quiet and practical rather than theatrical. We see growing adoption of AI-enabled tools for process optimization, yield improvement, and predictive maintenance—especially in complex chemistries, where small variations can have disproportionate effects. Digital twins, advanced process analytics, and data-driven scale-up models are moving steadily from experimentation into routine use.

Equally important is the digital transformation of quality systems and supply planning. AI-assisted deviation analysis, inspection-readiness platforms, and more sophisticated demand-forecasting tools are helping organizations reduce cycle times and make better decisions under uncertainty. Our own experience suggests a simple truth: technology creates value only when it is implemented in harmony with regulatory expectations and human judgment. In 2026, competitive advantage will not come from adopting AI quickly, but from adopting it thoughtfully and at scale.