Solid Dosage Drugs: Keeping Pace in New Drug Approvals

Solid dosage drugs are a steady segment in the global bio/pharma industry, but how do they measure in new drug approvals? A look at the dosage forms of new drug approvals thus far in 2026 and the market potential of some key solid dosage drugs.

Dosage forms and new drug approvals

The active pharmaceutical ingredient (API) is the key element in evaluating new drug approvals with the dosage form supporting the delivery of the API, but what trends in dosage forms can be observed from new drug approvals thus far in 2026? On a dosage-form level, solid dosage forms (i.e., tablets and capsules) are holding their own, accounting for 12 or 45% of the new drug approvals thus far in 2026, and of these drugs, which ones are of particular note?

Through July 16, 2026, the US Food and Drug Administration’s Center for Drug Evaluation and Research (CDER) had approved 26 new molecular entities and new biological therapeutics. Keeping to recent trends, new molecular entities (small-molecule drugs/chemically synthesized drugs) approved under new drug applications (NDAs) have accounted for the majority of new drug approvals by FDA’s CDER. CDERs reviews and approves new molecular entities under new drug applications (NDAs) and new biological therapeutics (eg., recombinant proteins, monoclonal antibodies and other antibodies) under biologics license applications (BLAs). Other biologic-based products, including blood products, vaccines, allergenics, tissues, and cellular and gene therapies, are reviewed and approved by a separate center within FDA, the Center for Biologics Evaluation and Research (CBER) and are not part of this analysis.

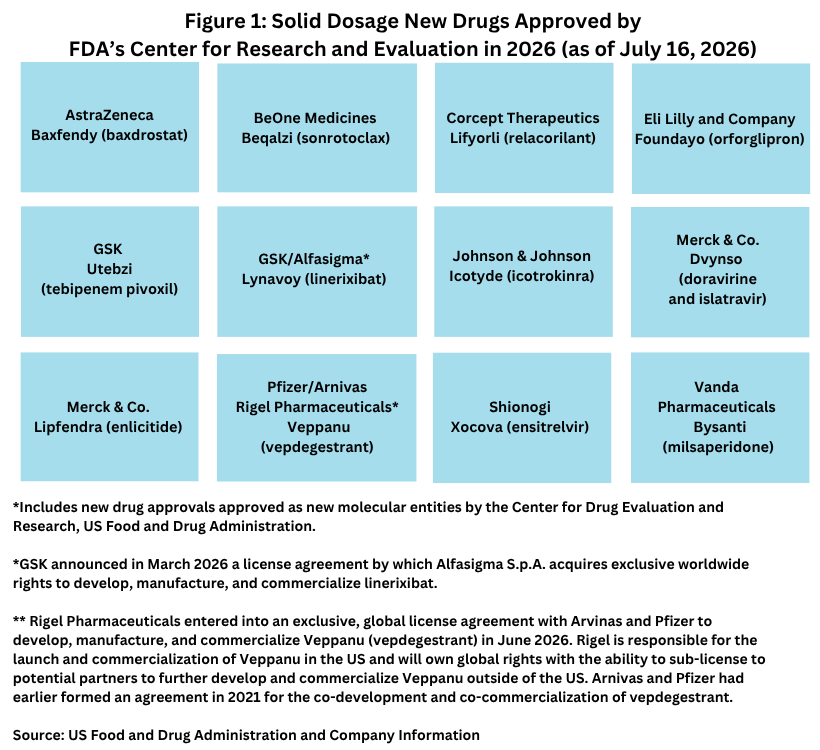

Thus far in 2026, NDA approvals have accounted for 19 new drug approvals or 73% of CDER’s approvals and BLAs for nine approvals or 27%. Table I at the end of the article outlines the new drug approvals by FDA’s CDER to date (July 16, 2026) and the dosage form/routes of administration for these drugs, Figure 1 below outlines the 12 new drugs with solid dosage forms approved by FDA’s CDER in 2026 to date,

Solid-dosage new drugs to watch

In looking at NDAs and the new drug approvals with solid-dosage forms, several new drug approvals stand out in terms of their potential market position.

On top of the list is Eli Lilly and Company, an addition to the company’s obesity drug portfolio with the approval of Foundayo (orforglipron), an oral obesity drug approved by FDA in April (April 2026) and in late-stage development for treating Type 2 diabetes. Foundayo is a once-daily small-molecule (non-peptide) oral glucagon-like peptide-1 (GLP-1) receptor agonist (RA). Analysts project blockbuster potential (defined as sales of $1 billion or more) for the drug with the oral administration being a key driver for revenue potential. In a recent analysis, Clarivate projects sales of orforglipron of $11.1 billion for obesity in 2031 in the G7 markets (Canada, France, Germany, Italy, Japan, the UK, and the US) and $5.2 billion in expected sales for Type 2 diabetes in the G7 markets in 2031. Orforglipron is the first oral, non-peptide, small-molecule GLP-1 RA to be approved. It can be taken without food or water restrictions at any time of the day. As such, it represents a breakthrough in convenience and accessibility compared with injectable alternatives, according to the Clarivate analysis.

This week (July 16, 2026), Merck & Co. received FDA approval for Lipfendra (enlicitide), an drug for treating certain forms of high cholesterol, and where oral administraton is a differentiator over existing drugs. The drug was approved to reduce low-density lipoprotein cholesterol (LDL-C) in adults with hypercholesterolemia (i.e., high cholesteroal), including heterozygous familial hypercholesterolemia (HeFH), an inherited genetic disorder that causes high cholesterol levels. Lipfendra is a macrocyclic peptide and is the first FDA-approved oral proprotein convertase subtilisin kexin type 9 (PCSK9) inhibitor shown to lower LDL-C, also known as bad cholesterol.

Analysts project potential blockbuster status for Lipfendra with potential peak sales of $4 billion to $5 billion by 2034. Lipfendra will competer with other PCSK9 inhibitors on the market, all of which are injectables: Novartis’ Leqvio (inclisiran); Amgen’s Repatha’s (evolocumab); and Regeneron Pharmaceuticals’/Sanofi’s Praluent (alirocumab). Among these drugs, Amgen’s Repatha was the highest market performer with 2025 sales of $3.0 billion, followed by Novartis’ Leqvio with 2025 sales of $1.2 billion, and Regeneron’s/Sanofi’s Praulent with combined 2025 revenues from the two companies of $844 million.

Johnson & Johnson (J&J) received FDA appoval for Icotyde (icotrokinra), a once-daily oral peptide and interleukin-23 (IL-23) receptor antagonist for treating moderate-to-severe plaque psoriasis. Along with J&J’s Tremfya (guselkumab), an injectable, Icotyde is positioned as a non-injectable alternative and potential successor to J&J’s blockbuster drug, Stelara (ustekinumab), once J&J’s top-selling drug, which faces biosimilars competition. In 2025, global sales of Stelara declined to $6.08 billion, representing an approximately 41% decline year-over-year, and in the first half of 2026, sales declined to $1.40 billion, a 57.4% decline year over year. Icotyde is also being studied in the other indications of Stelara: active psoriatic arthritis, moderately-to-severely active ulcerative colitis and moderately-to-severely active Crohn’s disease. Clarivate projects expected sales of Icotyde of $1.5 billion in the G7 markets in 2031.

Another solid-dosage drug with potential blockbuster status is Pfizer’s/Arvinas’/Rigel Pharmaceuticals’ vepdegestrant, an oral medication designed to treat estrogen receptor (ER)-positive, human epidermal growth factor receptor 2 (HER2)-negative (ER+/HER2-) advanced breast cancer. It was approved in May (May 2026) as the first PROteolysis Targeting Chimera (PROTAC) protein degrader. Designed to target and degrade the estrogen receptor protein, early studies suggest PROTAC-induced degradation is more complete than with oral selective estrogen receptor degraders, thereby potentially overcoming endocrine resistance in breast cancer. Potential label expansions include the drug in combination with another breast cancer drug by Pfizer, Ibrance (palbociclib).

In June (June 2026), Rigel Pharmaceuticals entered into an exclusive, global license agreement with Arvinas and Pfizer to develop, manufacture, and commercialize Veppanu (vepdegestrant). Rigel is responsible for the launch and commercialization of Veppanu in the US and will own global rights with the ability to sub-license to potential partners to further develop and commercialize Veppanu outside of the US. Arnivas and Pfizer had earlier formed an agreement in 2021 for the co-development and co-commercialization of vepdegestrant.

AstraZeneca’s Baxfendy (baxdrostat) also shows strong market potential. It is an oral, small-molecule aldosterone synthase inhibitor (ASI) for the treatment of hypertension in combination with other antihypertensive medications, to lower blood pressure in adults whose blood pressure is not adequately controlled. Baxfendy is an ASI designed to lower blood pressure in a new way by specifically inhibiting the production of aldosterone, a hormone that raises blood pressure to unhealthy levels and increases the risk of heart and kidney problems. As part of a broad development program, Baxfendy is also being investigated in clinical trials in other conditions where high aldosterone plays a role in elevating cardiorenal risk, including as a monotherapy for primary aldosteronism, and in combination with dapagliflozin for chronic kidney disease and hypertension and the prevention of heart failure in patients with hypertension. AstraZeneca acquired Baxfendy through its acquisition of CinCor Pharma. in 2023. Analysts project potential blockbuster status in 2029 of $1.3 billion and potential peak sales of $3.2 billion to $5.2 billion. in 2032.

Table 1: Dosage Forms/Route of Adminitrations of New Drug Approvals in 2026 by FDA’s Center for Drug Evaluation and Research (as of July 16, 2026)

| Company | Branded Name (active pharmaceutical ingredient) | Type of Filing | Dosage form; Route of administration | Indication |

| AbbVie | Decnupaz (pivekimab sunirine-pvzy) | BLA | Lyophilized cake; Intravenous infusion | Blastic plasmacytoid dendritic cell neoplasm, a rare hematologic malignancy |

| Acrotech Biopharma/ Evive Biotech | Adquey (difamilast) | NDA | Ointment; Topical | Mild-to-moderate atopic dermatitis (eczema) |

| Ascendis Pharma | Yuviwel (navepegritide) | NDA | Lyophilized powder; Subcutaneous injection | To increase linear growth in pediatric patients 2 years and older with achondroplasia with open epiphyses |

| AstraZeneca | Baxfendy (baxdrostat) | NDA | Tablet; Oral | Hypertension in combination with other antihypertensive drugs |

| Bayer | Ambelvist (gadoquatrane) | NDA | Solution; Intravenous injection | To detect and visualize lesions with abnormal vascularity, in conjunction with MRI |

| BeOne Medicines | Beqalzi (sonrotoclax) | NDA | Tablet; Oral | Relapsed or refractory mantle cell lymphoma |

| Celcuity | Revtorpyk (gedatolisib) | NDA | Lyophilized powder; Intravenous infusion | HR-positive, HER2-negative locally advanced or metastatic breast cancer |

| Corcept | Lifyorli (relacorilant) | NDA | Capsule; Oral | Platinum-resistant epithelial ovarian, fallopian tube, or primary peritoneal cancer |

| Denali | Avlayah (tividenofusp alfa-eknm) | BLA | Lyophilized powder; Intravenous infusion | Hunter syndrome (Mucopolysaccharidosis Type II) |

| Eli Lilly and Company | Foundayo (orforglipron) | NDA | Tablet; Oral | To reduce excess body weight and maintain weight reduction long term in adults with obesity or adults with overweight in the presence of at least one weight-related comorbid condition |

| Gilead Sciences | Hepcludex (bulevirtide-gmod) | BLA | Lyophilized powder; Subcutaneous injection | Chronic hepatitis delta virus infection in adults w/o cirrhosis or with compensated cirrhosis |

| GSK | Utebzi (tebipenem pivoxil) | NDA | Tablet; Oral | Complicated urinary tract infections |

| GSK/ Alfasigma* | Lynavoy (linerixibat) | NDA | Tablet; Oral | Cholestatic pruritus (severe itching) associated with primary biliary cholangitis (a rare liver disease) |

| Haisco | Cypsedo (cipepofol) | NDA | Emulsion; Intravenous injection (bolus) or infusion | To induce general anesthesia in adults undergoing surgery |

| Immedica Pharma | Loargys (pegzilarginase-nbln) | BLA | Solution; Intravenous infusion or subcutaneous injection | Hyperargininemia (rare liver disease) in adult and pediatric patients 2 years of age and older with Arginase 1 Deficiency |

| Johnson & Johnson | Icotyde (icotrokinra) | NDA | Tablet; Oral | Moderate-to-severe plaque psoriasis |

| Merck & Co. | Dvynso (doravirine and islatravir) | NDA | Tablet; Oral | HIV-1 infection |

| Merck & Co. | Lipfendra (enlicitide) | NDA | Tablet; Oral | To reduce low-density lipoprotein cholesterol in adults with hypercholesterolemia (high cholesterol) |

| Novo Nordisk | Awiqli (insulin icodec-abae) | BLA | Solution; Subcutaneous injection | Type 2 diabetes |

| Pfizer/ Arnivas/ Rigel* | Veppanu (vepdegestrant) | NDA | Tablet; Oral | Estrogen receptor-positive, human epidermal growth factor receptor 2-negative, ESR1-mutated advanced or metastatic breast cancer |

| Sentynl | Zycubo (copper histidinate) | NDA | Lyophilized powder; Subcutaneous injection | Menkes disease, genetic disorder affecting the body’s ability to process copper. |

| Shionogi | Xocova (ensitrelvir) | NDA | Tablet; Oral | Post-exposure prophylaxis of coronavirus disease 2019 (COVID-19) |

| Vanda Pharma | Bysanti (milsaperidone) | NDA | Tablet; Oral | Schizophrenia and manic or mixed episodes associated with Bipolar I disorder |

| Vera | Trutakna (atacicept-vymj) | BLA | Solution; Subcutaneous injection | Proteinuria (protein in urine) in adults with primary immunoglobulin A nephropathy |

| Viridian | Lumvoa (veligrotug-vvze) | BLA | Solution; Intravenous infusion | Thyroid eye disease |

| Wockhardt | Zaynich (cefepime and zidebactam) | NDA | Lyophilized powder; Intravenous infusion | Complicated urinary tract infections |

*GSK announced in March 2026 a license agreement by which Alfasigma S.p.A. acquires exclusive worldwide rights to develop, manufacture, and commercialize linerixibat.

** Rigel Pharmaceuticals entered into an exclusive, global license agreement with Arvinas and Pfizer to develop, manufacture, and commercialize Veppanu (vepdegestrant) in June 2026. Rigel is responsible for the launch and commercialization of Veppanu in the US and will own global rights with the ability to sub-license to potential partners to further develop and commercialize Veppanu outside of the US. Arnivas and Pfizer had earlier formed an agreement in 2021 for the co-development and co-commercialization of vepdegestrant.

Source: US Food and Drug Administration